Wavelet Applications in Economics & Finance

Using R studio & Matlab

Place Dates Price & Registration deadline

New Delhi, India 19-20 Dec. 2019

Hotel Swati Deluxe, New Elhi

Istanbul, Turkey 24-25 Jan. 2020

Movenpick, Levent

Beijing, China 07-08 Mar. 2020

Regus Beijing, China life-West

Kedah, Malaysia

Post-2020 GEC Conference 28 May. 2020 480 Malaysian Ringgit, 15 Apr. 2020

UUM University campus

M&S Research Hub organizes a 2-day workshop about Wavelet analysis for bankers, financial analysts, brokers, junior and experienced researchers in the fields of Economics & Finance.

Wavelet-based analysis is a POWERFUL TOOL for

Researchers who work on high-frequency time series data and are willing to decompose this data into signals of different time scales before applying econometric techniques to analyze them.

Bankers, investors, and financial analysts who deal with timely-sensitive data and rely on forecasted stock prices to make decisions regarding buying, selling or holding the stock or to change their portfolio accordingly.

Economists and policymakers who use forecasts of economic variables such as GDP, inflation, housing price, etc to define policy actions and draw important inferences.

About the Wavelets

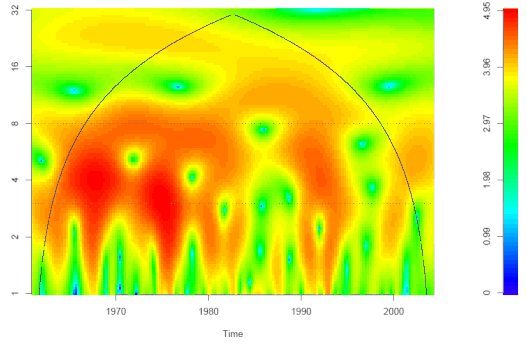

Wavelet Analysis is a powerful tool for compressing, processing, and analyzing data. It can be applied to extract useful information from numerous types of data, including images and audio signals in Physics, Chemistry, and Biology, and high-frequency time series in Economics and Finance.

The last few decades have been an era of big data, especially for the field of Finance, as many financial variables such as stock prices now can be measured in very high frequency - on minute-basis or even second basis. Financial data sets become huge, featuring large volume as well as high variability and complexity. More than ever, this increasing sophistication calls for the need of data processing tools.

Scholars, investors, financial analysts, and experts in the field yearn for mathematical theories and applications that can help them make sense of all the information presented in the data and use that information to improve their understanding of financial systems or just simply to take the right decisions.

This methodology studies the temporal and frequency information of time series data simultaneously. Wavelet transform utilizes local base functions that can be stretched and translated with a flexible resolution in both frequency and time.

These techniques are particularly useful for managing transient and non-stationary time series data and to locate discontinuities in such data. Given the highly useful implications of wavelets, over the past 20 years, applications of these methods have been rapidly adopted by researchers and industrial practitioners who deal with real-world time series data.

Content of the workshop

This workshop provides an excellent opportunity for scholars, bankers, and industrial data practitioners to learn and enhance their knowledge about Wavelet methods using R programming and Matlab. Over two days, the workshop will cover an extended list of topics

DAY-1

1. Introduction to R-Programming Language and R-studio Interface

2. The basic concept of Wavelet and its applications

3. Decomposition and plotting of the series using the MODWT method.

4. Wavelet Correlation

5. Wavelet Covariance

6. Cross-Wavelet Correlation

DAY-2

1. Continuous Wavelet Transform

2. Cross Wavelet Transform

3. Wavelet Coherence

4. Partial Wavelet Coherence

5. Introduction of MATLAB

6. Application of Continuous Wavelet Transform, Wavelet Coherence, Partial and Multiple Wavelet Coherence (Using MATLAB)

Organization of the workshop

- Language of instruction: English

- Certificate of enrollment

- Registration fees include the workshop material and data files

- The workshop starts every day from 1 PM until 5 PM

The workshop setting is highly interactive and includes real-life data applications on R and Matlab. The workshop content is designed to meet all levels of proficiency, accordingly no prior knowledge of R, Matlab and Wavelets are needed. However, a basic knowledge of statistical and econometric methods is required.

Workshop Speaker

Dr. Asrhian Sharif

With more than 800 citations, an RG score that exceeds 29, and a huge experience, Asrhian Sharif stands as one of the leading researchers in using wavelet-transform techniques in analysis and research methods. His publications' profile is multidisciplinary and involves articles at top-notch journals such as Journal of Cleaner Production 5.56, Renewable Energy 4.90, Energy Policy 4.14, Current Issues in Tourism 3.45, and Physica 2.142.

Arshian is a lecturer at Universiti Utara Malaysia and before he was a lecturer and a manager of the research and publications department at Iqra University.

Do you have any questions?

Contact us at events@ms-researchhub.com

Chat with us during our working hours

Monday-Friday 10 AM-4 PM

M&S Research Hub / Copyright © 2018-2025

Tax ID (Germany): 026 825 34113 - EU/ID: DE324037141

Highlights

Get in Touch

+49 017686387586

Chat

Mo-Fri: 9 AM-4 PM